For most of the twentieth century, economics relied on "experiments that happen to occur" (Friedman, 1953, p. 10). But, something transformational happened in 1955 at Purdue University. A newly minted Assistant Professor named Vernon Smith, stressed with a 4-4 teaching load, had insomnia and reflected on an experiment he had participated in at Harvard. In Chapter 9 of Papers in Experimental Economics, Smith writes about an episode of insomnia,

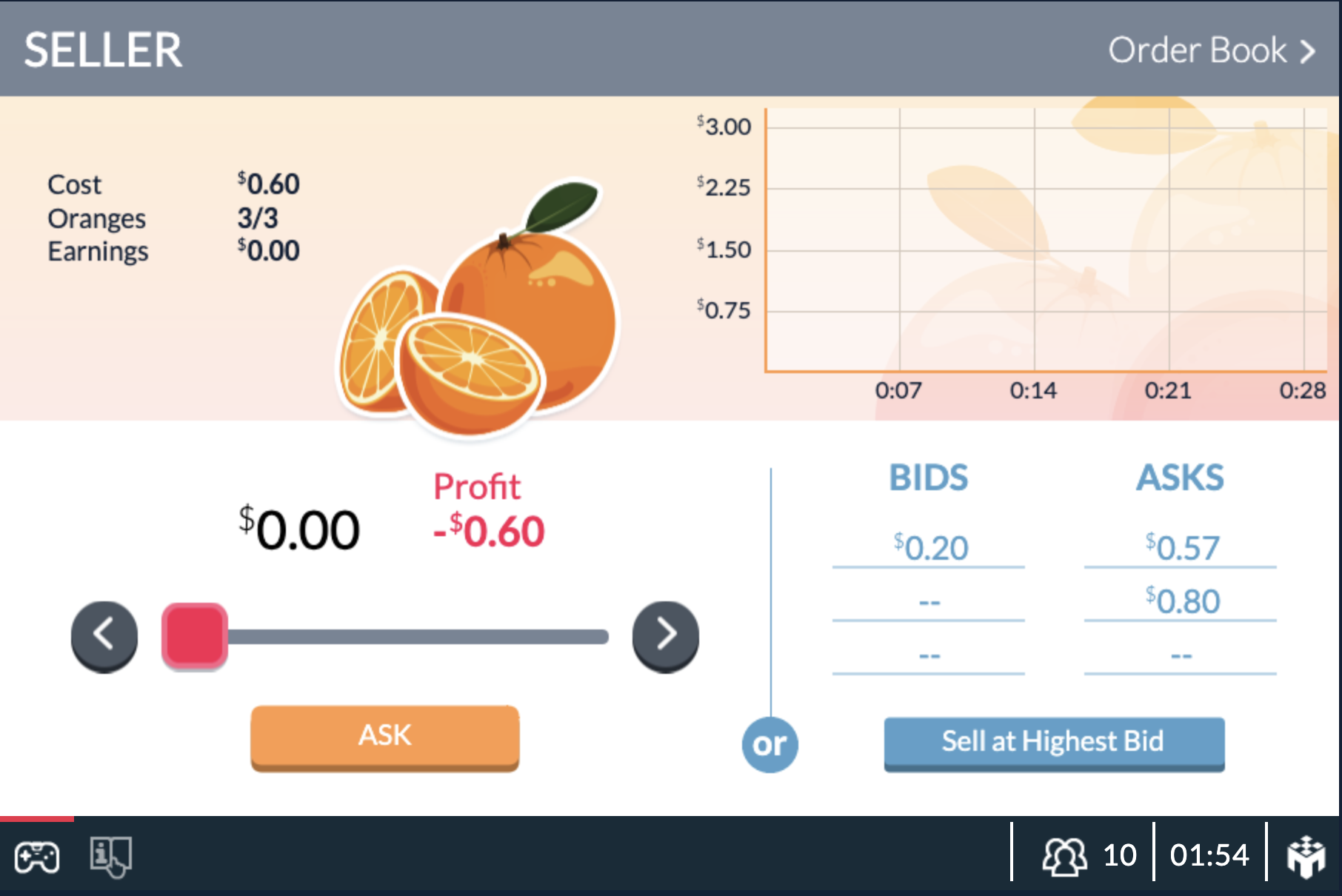

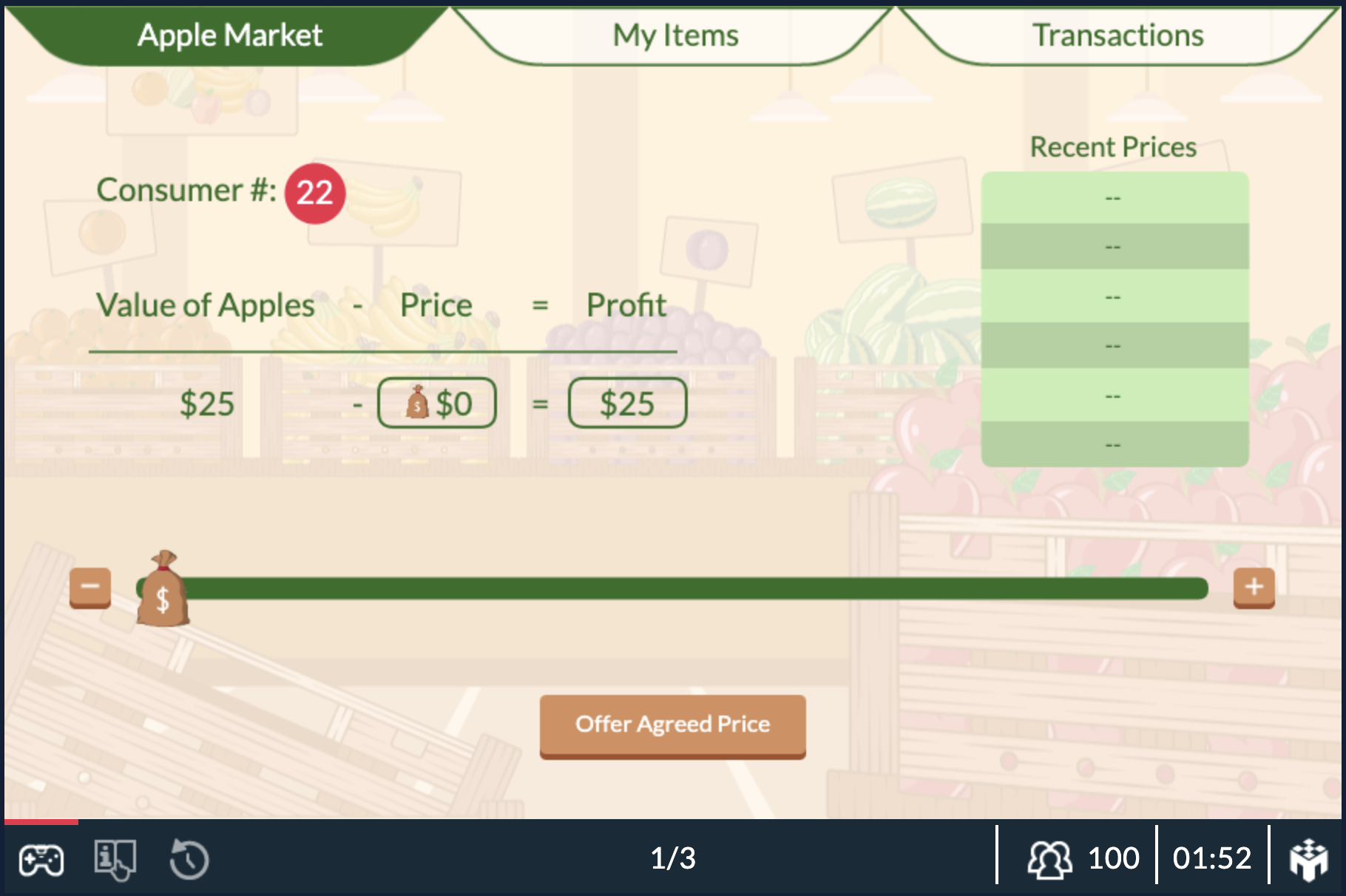

With MobLab's online economics games you can actually recreate this episode in history. You can have the students participate in one period of trade in our "Pit Market" and multiple periods of trade in our "Competitive Market." What this would help emphasize is that (1) the trading rules matter; (2) there is learning involved in trading and that equilibrium price is something that is tended towards, and (3) equilibrium can be reached with even weaker assumptions than needed by theory.

"So there I was, wide-awake at 3 am, thinking about Chamberlin's "silly" experiment. He gave each buyer a card with a maximum buying price for a single unit, and each seller a card with a minimum selling price for one unit. All of us were instructed just to circulate in the room, engage a buyer (or seller), negotiate a contract, or go out to find another buyer (or seller) and so on. If a buyer and a seller made a contract, they were to come to Chamberlin, reveal the price of the exchange, turn in their cards, and he would post the price on the blackboard for all to see. When it was all over, he would reveal the implicit demand and supply schedules, and we would learn the important lesson that supply and demand theory was worthless in explaining what had happened; namely that prices were not near the equilibrium and neither was the quantity exchanged. The thought occurred to me that the idea of doing an experiment was right, but what was wrong was that if you were going to show that competitive equilibrium was not realizable...you should choose an institution of exchange that might be informationally more favorable to yielding competitive equilibrium. Then when such an equilibrium failed to be approached, you would have a powerful result. This led to two ideas: (1) Instead of having the subjects circulate and make bilateral deals, why not use the double oral auction procedure, used on the stock and commodity exchanges? (2) Since Marshall had talked about a competitive equilibrium as simply a tendency ... why not conduct the experiment in a sequence of trading days in which supply and demand were renewed to yield functions that were daily flows?"The institution of exchange that would be "informationally more favorable to yielding a competitive equilibrium" was the double oral auction. In that institution buyers bid, sellers ask, and an auctioneer records the bids/asks in a public and centralized location. These were the rules of the NYSE. Unlike Chamberlain's one-shot pit market, the double oral auction produced outcomes that converged to equilibrium and multiple "trading days" helped to illustrate that students learned from day to day. Smith wrote of his thoughts at the time, "But, the results can't be believed, I thought. It must be an accident ..." Over the next several years Smith conducted several of these double oral auction markets at Purdue and Stanford with different supply and demand configurations. Markets converged. It turned out that markets didn't need to be "thick" to converge. Individuals didn't need to have information about other's valuation or cost schedules. Individuals didn't start out as price-takers. Rather those individuals started out buying and selling units at a positive profit and the forces of diminishing marginal utility, increasing marginal cost, and the public/central information on bids and asks pushed people to the point of indifference. What a glorious finding! It gives us confidence that there is an empirical basis for the supply and demand framework. This insomnia and classroom economics experiment started him on a path of research that eventually earned him the Nobel Prize in 2002 for, "having established laboratory experiments as a tool for empirical analysis, especially in the study of alternative market mechanisms." Now experimental methods and themes have permeated every major subfield in economics. At a more fundamental level Smith transformed economics from an observational science to an experimental science.

With MobLab's online economics games you can actually recreate this episode in history. You can have the students participate in one period of trade in our "Pit Market" and multiple periods of trade in our "Competitive Market." What this would help emphasize is that (1) the trading rules matter; (2) there is learning involved in trading and that equilibrium price is something that is tended towards, and (3) equilibrium can be reached with even weaker assumptions than needed by theory.